Luxury Homes Market 2024H2

Bungalow market activity picked up in 2024H2

Sales activity in the residential market moved at a faster pace in the second half or 2024 as seen in the robust take-up of new projects as well as the Good Class Bungalow (GCB) market. This could be attributed to improved sentiments due to the three rounds of interest rates cut by the US Federal Reserve. The first round was a 50-basis-point (bps) cut in September, followed by a reduction of 25 bps in November and finally, another cut of 25 bps cut in December.

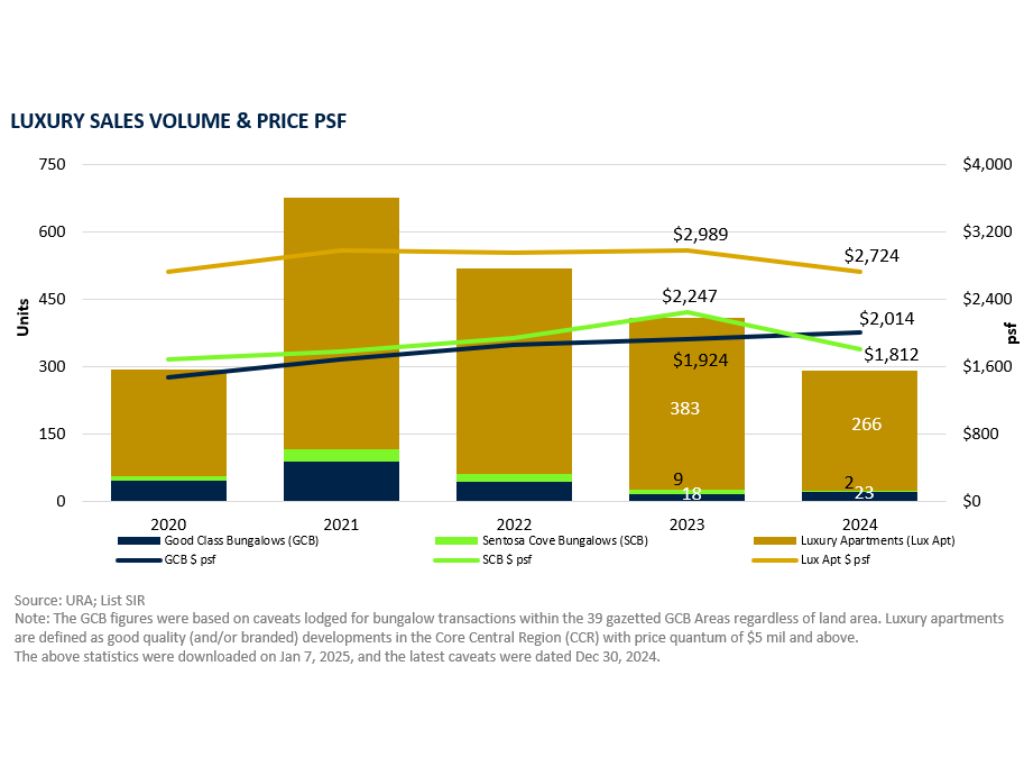

The interest rates cut induced confidence in home buyers and investors as it enhanced both affordability and the long-term value of real estate assets. There has been a noticeable flow of wealth into the GCB market since July 2024. Statistics provided by the URA showed that there were 14 bungalow deals in 2024H2, up from nine deals each in the first half of the year and in 2023H2.

The total tally of 23 GCBs sold in 2024 clearly outperformed the 18 deals done in 2023. Hence the total investment value of $652.05 mil for 2024 is 51% higher than the $432.51 mil achieved in 2023.

Unfortunately, the positive sentiment was not seen in the bungalow market at Sentosa Cove. Statistics showed that only two transactions took place in the whole year, the lowest sales volume since 2008, when there was only one sole transaction. The lacklustre performance at Sentosa Cove could be attributed to the absence of foreign purchasers who were hit by the hike in the additional buyer’s stamp duty (ABSD) from 30% to 60% with effect from 27 April 2023. The slowdown began since 2023H2 with two bungalow deals, trickling down to one each in the first and second half of 2024.

The two bungalows at Sentosa Cove were sold for a total of $30.16 mil which works out to $1,812 psf on land area.

The luxury apartments market also did not perform as well as in 2023. The 125 units sold in 2024H2, was lower than the 141 units sold in 2024H1 and 167 units sold in 2023H2. While the hike in ABSD kept foreign buyers away, the absence of significant new luxury projects launched in the Orchard Road area resulted in a drop of 30% in the 2024 sales volume compared to 2023. The total investment value of $1.96 billion reflects $2,724 psf, which is 9% lower than the average price of $2,908 psf for the deals done in 2023.

Advanced estimates by the Ministry of Trade and Industry (MTI) showed that the Singapore economy expanded by 4% in 2024, supported by broad-based growth across the goods-producing and services sectors. For 2025, MTI expects Singapore’s economy to grow by 1 to 3 per cent in view of challenges coming from a more protectionist global economic landscape. Nevertheless, geopolitical conflicts and trade wars could make Singapore more attractive as a safe haven for UHNWIs (ultra-high-net-worth individuals) from the USA, Europe and Asia. In 2025, we expect the GCB market to strengthen in 2025 and the luxury apartments segment to maintain its current performance. Challenges will remain for the Sentosa Cove bungalow market.

Good Class Bungalows (GCBs)

The GCB market had a slow start in 2024 with nine deals based on caveat data in the first six months. The slowdown started in 2023 due to the mismatch between buyers and sellers’ price expectations as well as the hike in ABSD in April 2024.

However, buying interest in GCB picked up from July 2024 onwards as some owners lowered their price expectations to more reasonable levels to entice buyers to return to the market. Still, the per square foot yardstick for GCB prices showed an increase 5% y-o-y to $2,014 psf. The downward correction of interest rates was another booster to the market. Between July and November, caveats for 14 transactions were lodged bringing the total to 23 transactions.

Besides these, another 12 GCB deals, totalling over $700 million, were reportedly completed this year without caveats lodged, as buyers sought anonymity. One such deal was the sale of a yet-to-be-completed bungalow at Tanglin Hill at the price of $93. 89 mil ($6,197 psf). It was the most expensive bungalow to be sold in 2024.

The sustained buying activity of this trophy asset through the year showed that GCBs are still coveted by the ultra-rich despite external economic factors. GCB prices are still rising because buyers have come to terms that prices of such highly sought-after properties would not ease. Most of the buyers in 2024 were a mix of self-made entrepreneurs, second or third generations of successful local business owners and new citizens.

Sentosa Cove Bungalows

Statistics provided by the URA showed that only two caveats were lodged for bungalow sales at Sentosa Cove in 2024. This is the lowest sales volume since 2008 when the Global Financial Crisis hit and only one bungalow was sold. In 2023, there were nine bungalow deals. The bungalow market at this resort island is largely dependent on the support of foreigners as it is the only location in Singapore where they are allowed to own landed homes.

The hike of ABSD from 30% to 60% for foreigners who buy residential property in April 2023 and the crackdown on money laundering activity in 2023Q3 were the main reasons for the stalemate at Sentosa Cove. Besides the two bungalows listed with URA, a third bungalow which belonged to one of the money launderers was put up for sale by the bank. Located at Ocean Drive, it is one of the rare big bungalow plots with a land area of 19,551 sq ft. After two failed attempts at auction, it was finally sold for $22 million ($1,125 psf).

Caveat data showed that the two bungalows in 2024 were sold to a Singaporean and a Singapore permanent resident (SPR). For comparison, the nine purchasers in 2023 were two foreigners, two SPRs and five Singaporeans.

The rental market was also facing challenges. Rental data showed that 24 bungalows were leased in 2024, down from 31 bungalows in 2023. The average rental for 2024 was $36,250 per month, whereas in 2023, it was $41,600 per month. We expect the sluggish sales in Sentosa Cove’s bungalow market to continue in 2025 unless sellers are prepared to accept lower offers for their homes.

Luxury apartments

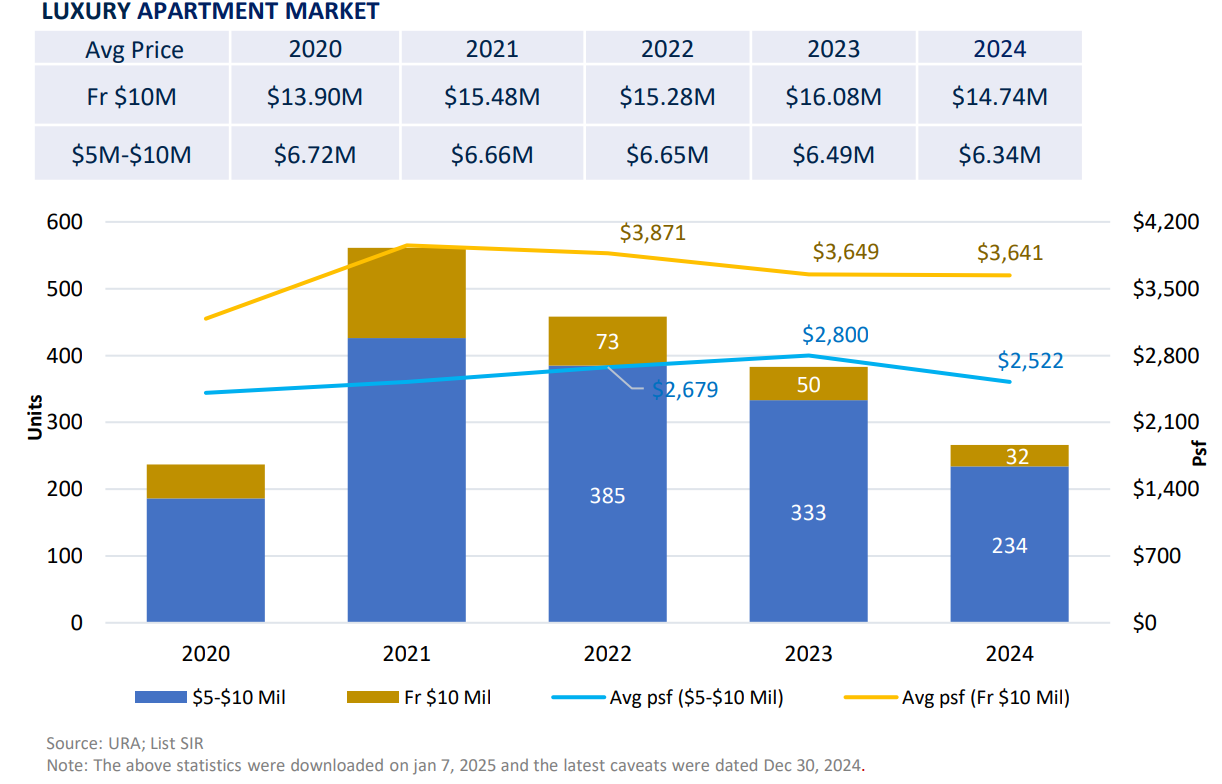

In 2024, the only new high-end projects were launched. The first is the 14-unit freehold Gilstead 32, which is located in district 11. All the units are of sizes from 3,800 sq ft to 4,200 sq ft and come with four bedrooms, quality fixtures and fittings. From its launch in April till the end of 2024, caveats showed that six units have been sold between $14.4 mil and $14.7 mil each. The second project is 99-year leasehold Skywaters Residences which is located at Prince Edward Road in the Downtown. The sole unit sold is also the most expensive unit sold in the year: a 7,761-sqft penthouse on the 57th storey that was bought by a foreigner for $47.34 mil ($6,100 psf). When completed, The Skywaters will comprise retail space (basement to level 2), Grade A offices (levels 3 to 22), Aman hotel (levels 24 to 26) and Skywaters Residences (levels 27 to 63).

Based on caveat data, 125 luxury apartments were sold in 2024H2, slightly lower than the 141 transactions in the first half of the year. The total sales volume of 266 units is 30% lower than the 383 units sold in 2023. The lower sales in 2024 could be attributed to the loss of foreign investors due to the hike in ABSD as well as the lack of new projects. As some 75% of the luxury apartments were resale properties, the average price softened by 9% y-o-y to $2,724 psf.

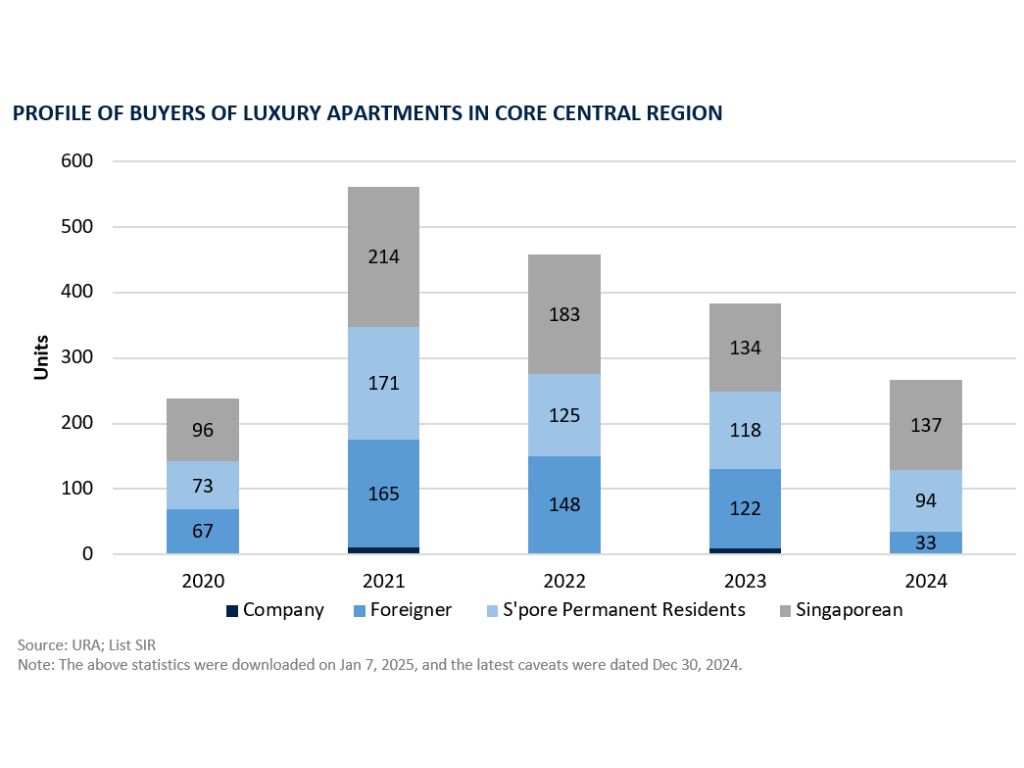

The profile of homebuyers in 2024 comprised 33 foreigners (12%), 94 PRs (35%), 137 Singaporeans (52%) and two purchases by company (1%). Compared with 2023, the 383 units were sold to 122 foreigners (32%), 118 PRs (31%), 134 Singaporeans (35%) and nine companies (2%). Clearly, there was a significant drop in the number of foreign and PR buyers in 2024.

The top five foreign investors (including PRs) in 2024 came from PRC, USA, India, Indonesia and Australia. In recent years, nationals from the USA have risen to become the second most active investors as it is one of the nations under the Free Trade Agreement which entitled them to be accorded the same stamp duty treatment as Singaporeans.

Rents in prime locations have been falling as confirmed by five consecutive quarters of decline in the rental index for Core Central Region (CCR). As at end of 2024, CCR rents have declined by 4.8% since end-2023. The highest rent achieved in 2024 was for a four-bedroom unit at The Marq On Paterson Hill for $80,000/ month. For comparison, the highest rent achieved in 2023 and 2022 had been $100,000/month for similar four-bedrooms in the same development. We expect to see more corrections in prime rents going forward. The positive outcome is that this could encourage more expatriates, who had moved to the suburbs due to the high rents in CCR during the pandemic, to relocate back to CCR.

Outlook

Of the three segments in the luxury residential market, the GCB market is expected to benefit from the rise of wealthy new citizens and the transfer of wealth to the second and third generations of local wealthy families. The bungalow market at Sentosa Cove would remain subdued unless prices are attractive enough to bring buyers back. As for the luxury apartment segment, the high ABSD will remain a deterrent to foreign buyers from countries without FTA with Singapore.